In part 1 of our December Crypto Regulation Recap, we explored the implications for crypto firms. Now, we turn our attention to how the updates impact banks and other regulated financial institutions (FIs), such as payment services providers (PSPs) and electronic money institutions (EMIs). Here, we focus more on the EU setting key industry standards.

European Union

1. Check MiCA licences and Travel Rule compliance

The frameworks for electronic money institutions and payment service providers are already established. The European Banking Authority (EBA) has provided an explainer to clarify the regulatory landscape for crypto asset service providers (CASPs).

Key requirements to keep in mind:

- CASPs that issue both asset-referenced tokens (ARTs, tokens pegged to assets) and e-money tokens (EMTs, tokens used to transfer value, similar to e-money) must be licensed to operate in the EU. MiCA outlines the main principles, but EU member states establish licensing regimes and requirements.

- Compliance with EU AML/CFT rules after getting a licence.

- Ensuring AML/CFT risks have been assessed and mitigated is also a requirement for ART issuers who are not CASPs.

- Complying with the Travel Rule requirements, i.e., including required information on the originator and beneficiary of crypto asset transfers. CASPs also have to apply specific measures to crypto asset transfers involving self-hosted addresses.

What is the impact on banks and other FIs?

Non-CASP financial institutions, such as banks, payment services providers, and electronic money institutions, will have to assess their CASP partners’ licensing status and requirements and their AML/CTF controls.

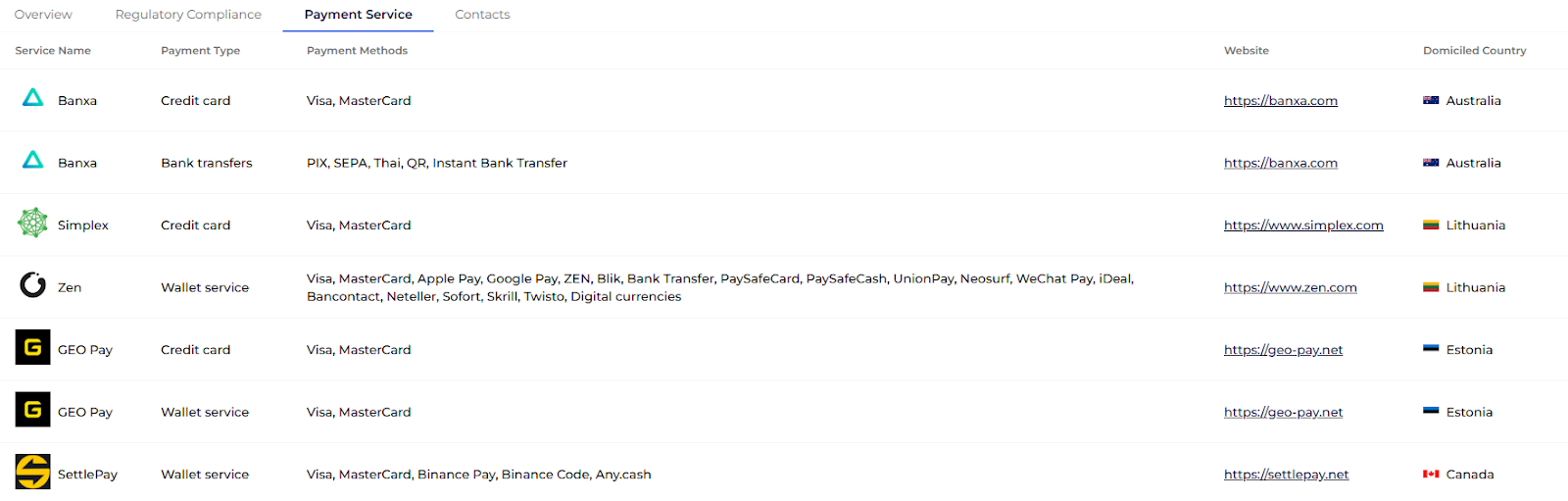

Checking CASPs regulatory compliance is easy with the GL Entity Explorer, an all-in-one overview of an entity.

Moreover, the tool contains data about payment services the entity supports:

2. Pay attention to the “grandfathering regime” for CASPs

Crypto firms operating in the EU before 30 December 2024 can continue their activities until 1 July 2026 (or a date set by national regulators, whichever is earlier) under the “grandfathering regime” while working toward full MiCA licensing. This regime covers a broad range of CASPs, including those issuing, trading, or providing services for crypto assets, beyond just custodial wallet providers and crypto-fiat exchanges.

For a specific period across EU member states, check out an ESMA list. Some countries, like Lithuania, set short periods (5 months), while others, including Czechia and France, allow up to 18 months.

! Please note: If a CASP operates in two countries with different MiCA transition periods, such as 12 months in one (Member State A) and 6 months in another (Member State B), it must consider the timeline in Member State B.

What is the impact on banks and other FIs?

Banks, PSPs and EMIs will have to understand specific grandfathering provisions in a relevant EU country when assessing their CASPs partners’ licensing status.

3. Check when a solution is provided for the overlap between MiCA and the Payment Services Directive

Under MiCA, EMT issuers require authorization, but certain CASP activities involving EMTs may unintentionally fall under PSD2 (Payment Services Directive).

The EU Commission clarified that CASPs offering EMT-based payment services must either obtain PSP authorization or partner with an authorized PSP, particularly for third-party or P2P transfers. However, CASPs acting as direct buyers or sellers of EMTs without handling transfers or intermediating payments do not require PSP authorization.

Situations where EMTs are used for trading or investment rather than payments may still inadvertently trigger PSD2 requirements, an issue the Commission has asked the EBA and ESMA to review.

What is the impact on banks and other FIs?

Banks are advised to assess the business models and the respective licensing requirements for their existing and potential partners and clients involved in EMTs.

4. Pay attention to the clarified reporting requirements for FIs under MiCA

The EBA has released templates, guidelines, and an explainer detailing the reporting requirements for ART and EMT issuers under MiCA. These documents apply to various entities, including credit institutions (like banks) and EMIs.

What is the impact on banks and other FIs?

Like CASPs, banks, EMIs, and PSPs involved in activities regulated by MiCA must understand the reporting templates and thresholds that apply to them. These requirements depend on their business model, the types of tokens they issue, and the countries they operate in. They should integrate these reporting obligations into their operations.

Argentina

5. Check the FATF mutual evaluation report on Argentina

The Financial Action Task Force (FATF) has issued a mutual evaluation report on Argentina, placing the country on “enhanced follow-up.” It will have to report back to the FATF within a year. The report highlights the role of VASPs as reporting entities for AML and CTF purposes and examines their involvement in asset recovery and investigations.

What is the impact on banks and other FIs?

Financial institutions should use the FATF mutual evaluation report on Argentina as a prompt to review the country’s risk rating in their compliance systems. Banks and regulated entities with crypto partners in Argentina should reassess these partners’ adherence to AML/CTF reporting obligations.

Any questions about adjusting to the regulations for banks and financial institutions? Feel free to contact us.