Key insights:

- Set to be enacted in 2026, DAC8 extends EU tax reporting requirements to the crypto sector, targeting both regulated and unregulated entities, and mandating records of crypto transactions and user information for enhanced transparency and tax evasion prevention.

- Crypto service providers and operators will face significant reporting duties, covering different forms of crypto transactions, including cross-border and domestic transfers, exchanges, and payments.

- The directive encompasses a wide range of crypto assets, including currencies like Bitcoin and Ether, stablecoins, digital representations of fiat currencies, and even NFTs used for payments or investments.

- Crypto businesses must retain transaction records for 5–10 years.

- Non-compliance will lead to enforcement actions determined by EU members’ regulatory authorities.

In about two years, the DAC8 directive is set to become law. It means the crypto space will also have to comply with its requirements. What exactly does the document propose, and how will it impact crypto businesses? Let’s break it down.

DAC8 focuses on tax income derived from crypto transactions

DAC stands for the Directive on Administrative Cooperation, which provides the rules and procedures for the automatic exchange of information between EU members’ tax authorities. The number 8 refers to the proposed eighth amendment to the document, which has gone through a series of updates.

So, DAC8 is a further revision of these directives, which now includes an automatic exchange of information in the area of crypto assets and e-money. Its main goal is to increase transparency and prevent tax evasion in crypto transactions within the EU by extending tax reporting and information exchange requirements.

The directive brings new responsibilities to crypto businesses

- Reporting obligations are set for regulated and non-regulated providers and operators

Financial institutions are mandated by the previous Directive 2011/16/EU to report account information for tax purposes. The DAC8 extends this requirement to include crypto assets and their service providers* and operators**, which were not previously covered.

! DAC8 applies to both regulated crypto asset service providers (centralized exchanges like Binance or Coinbase) and non-regulated ones (decentralized exchanges, for example, Uniswap). They are collectively referred to as reporting crypto asset service providers (RCASP).

*Crypto asset service providers are entities regulated by and authorized under Regulation (EU) 2023/1114. They include businesses that provide various services related to crypto assets, such as exchanges, wallet providers, and others involved in the trading, transfer, and management of cryptocurrencies and related digital assets.

**Crypto asset operators include entities that are not regulated under the above-mentioned document but are still involved in crypto asset services. They could be entities engaged in similar activities as service providers but not falling under the specific regulatory framework of the regulation, for instance, peer-to-peer exchange platforms allowing for direct transactions between users.

- Wealthiest individuals fall under the law

Advance cross-border tax rulings include those involving high-net-worth individuals. However, the key factor is actually not wealth, but how much money is involved in the transaction or series of transactions. Specifically, if the amount is more than €1,500,000 (or its equivalent in another currency), then it’s relevant.

! Please keep in mind that the document doesn’t explicitly mention a specific time period over which this transaction amount should be calculated.

- The directive includes various types of crypto assets

- Decentralized assets, such as Bitcoin, Ether, and others

- Stablecoins, which are pegged to a reserve asset like USDT

- E-money tokens representing electronic money, e.g., a digital representation of fiat currency

- NFTs that can be used as a means of payment or for investment

- Other digitalized financial assets, for example, tokenized versions of traditional financial assets (stocks, bonds, or real estate).

4. Reportable transactions include exchange, transfer, and retail payment

Under DAC8, the following types of transactions must be reported:

- Crypto-fiat and crypto-crypto exchange

- Crypto transfers

- Crypto payments for goods or services, with a transaction value of $50,000+ or its equivalent in other currencies.

5. Both domestic and cross-border transactions must be reported

Also, the directive isn’t limited to typical buy-and-sell transactions. It also includes other activities, such as the exchange of crypto assets for other assets (digital or physical), transfers between wallets, and other forms of trade or transactions involving crypto.

6. Reporting crypto asset service providers have to submit transaction details and user/provider information

User and entity identification

For each reportable user*: name, address, member state(s) of residence, tax identification number (TIN), and for individuals, the date and place of birth.

! Countries in the EU need to make sure they collect and share TINs of people and businesses. To help do this, the commission will create a tool to check these numbers.

For any entity identified as having controlling persons who are reportable persons: the entity’s name, address, member state(s) of residence, TIN, and similar details for each controlling person.

GL screen with entity details and compliance information

*A reportable user is a person or entity using crypto services who needs to be reported for tax reasons and is an EU resident.

- Service provider identification

The name, address, TIN, individual identification number (if available), and global legal entity identifier of the reporting crypto service provider.

- Transaction details

It includes:

- The full name of each type of reportable crypto asset involved in transactions

- The total amount, the total number of crypto units, and the total number of buying and selling transactions involving fiat currency

- Overall market value, the total number of crypto units, and the total number of buying and selling transactions involving other cryptocurrencies

- Overall market value and the total number of crypto units used in transactions where cryptocurrencies are used to buy goods or services

- Overall market value, the total number of crypto units, and the total number of transactions for sending and receiving cryptocurrencies categorized by the type of transfer when known.

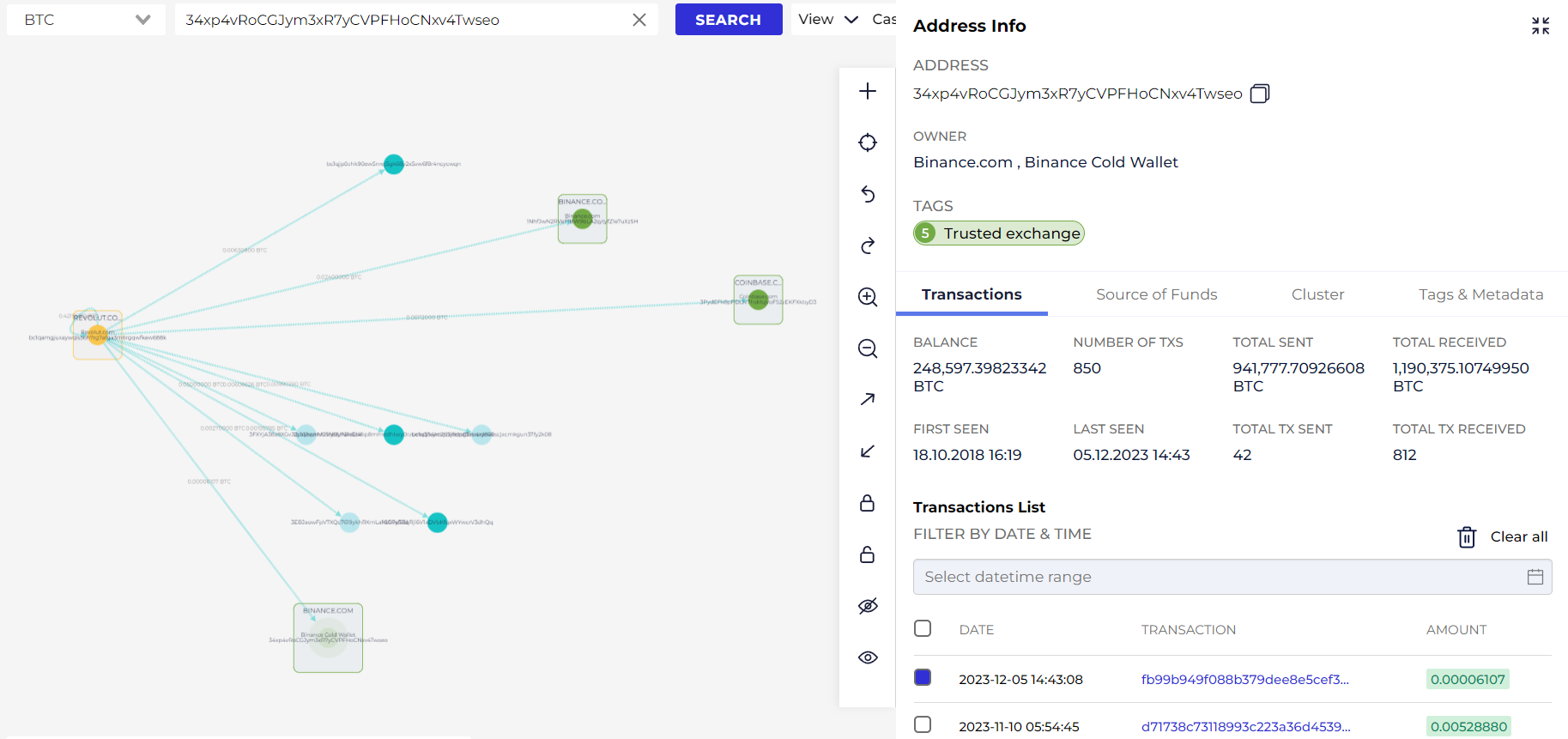

GL screenshot with information about transactions connected to the Binance hot wallet, with the number of transactions, balance, and last activity

7. Records should be kept for at least five years

Crypto asset service providers must maintain records of the steps taken and information used for reporting and due diligence for at least five years but not more than ten years after the reporting period.

The deadline to incorporate new rules is Dec 31, 2025

DAC8 comes into effect on January 1, 2026. This gives enough time for setting up the required regulations and putting the Markets in Crypto-Assets (MiCA) rules into action, which helped in getting DAC8 ready.

So, countries in the EU have time until December 31, 2025, to get these new rules into their own laws. This step-by-step process is designed to make sure everything is ready and runs smoothly.

Non-compliance may result in sanctions

- For service providers

EU countries must make sure these providers are doing their reporting correctly. If not, the states should take special steps (identified by these states’ watchdogs).

- For operators

If an operator does not comply with reporting obligations after two reminders, the state of registration must take measures to revoke its registration. It can happen no later than 90 days after the second reminder.

If they don’t meet the necessary conditions, or if their registration is canceled, the EU member state can remove them from the register.

- For users

If a user doesn’t give the required information even after being reminded twice and 60 days have gone by, then the service provider has to stop them from doing any transactions that would need to be reported.

DAC8 has pros and cons for crypto businesses and regulators

| Crypto businesses | Regulators | |

| Pros | Enhanced legitimacy | Consumer protection |

| Market stability | Closing the tax gap | |

| Clarity and predictability | Adapting to digital future | |

| Increased investor confidence | Harmonizing regulations | |

| Cons | Increased costs | Enforcement challenges |

| Reduced flexibility | Rapidly evolving sector | |

| Barrier to entry | Risk of stifling innovation |

The directive stresses the importance of lessening administrative tasks for crypto businesses. The reporting process needs to be clearly-defined, efficient, and simple. This is where blockchain analytics companies come into play. By using advanced tools and technologies, they can streamline and simplify complex data, ensuring that reporting is both accessible and precise.

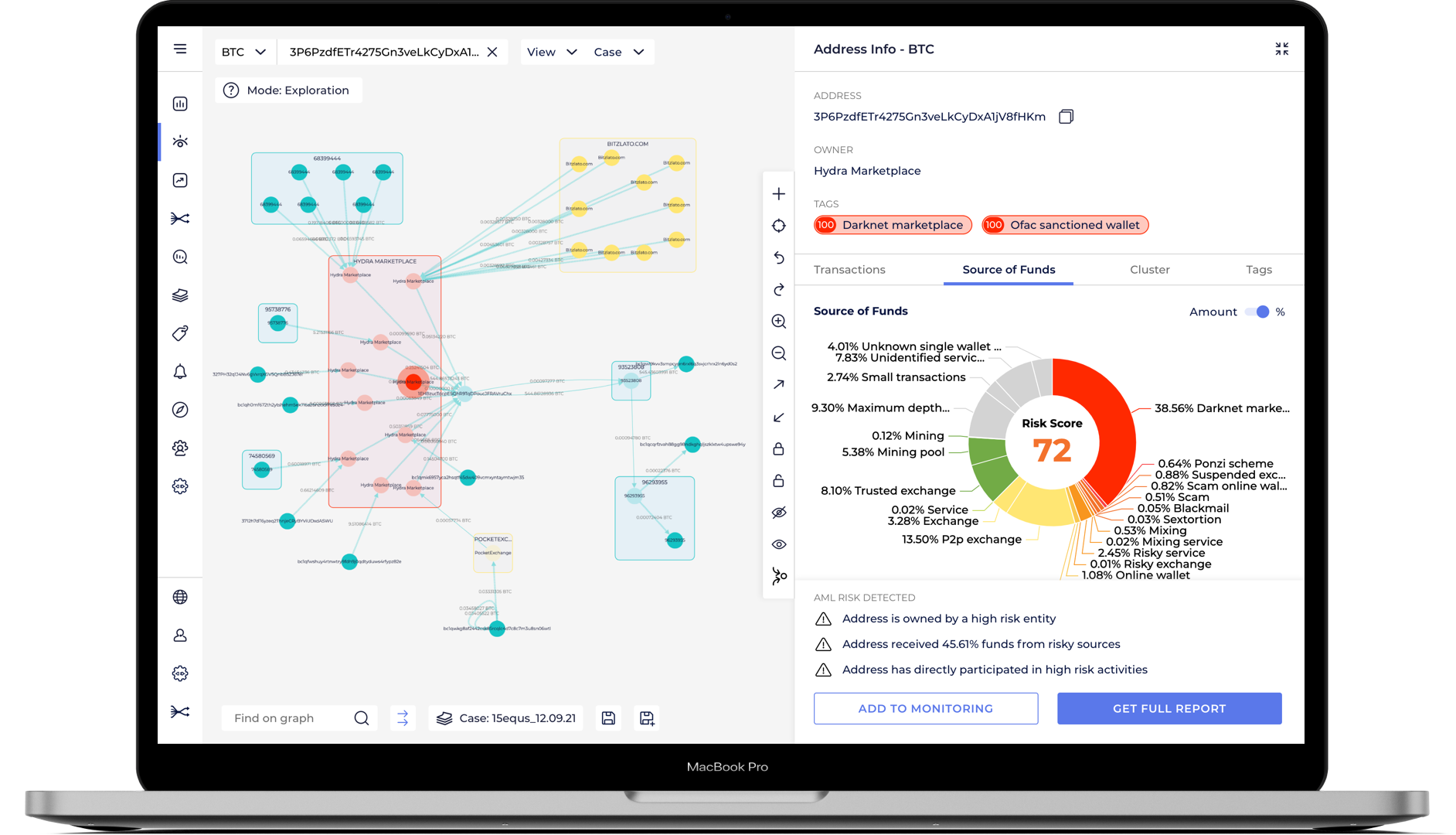

GL Vision screenshot with comprehensive data about the address, its owner, source of funds, transactions, and clusters

DAC8 is a big change for everyone in the crypto space in the EU

This new rule means crypto companies will have to report lots of details about their transactions and who is making them. While this could make the crypto market seem more trustworthy and stable, it also means more work and possibly higher costs for these companies.

Regulators will have an easier time watching over the market and making sure taxes are paid, but they’ll also have to keep up with a market that is always changing.

The effectiveness of DAC8 will depend on how well everyone involved can work together to maintain a secure and trustworthy financial market while still encouraging new ideas and growth.